In an industry where data is paramount, the lack of standardized protocols has long been a barrier to efficiency and innovation. The recently released white paper by the open Insurance Data Standards (openIDS) initiative sheds light on this challenge and introduces a transformative framework designed to revolutionize data interoperability across the insurance sector.openIDL

Key Highlights from the White Paper:

The Data Challenge: The insurance industry relies heavily on data for risk assessment, pricing, claims management, and customer engagement. However, the absence of universally adopted data standards has led to fragmented systems, increased operational costs, and hindered collaboration among stakeholders.openIDL

The Problem: Without common data standards, insurers expend significant resources translating data for various purposes, including regulatory reporting and catastrophe modeling. This inefficiency not only escalates costs but also impedes timely and accurate data exchange, affecting decision-making processes.openIDL

It’s Time for Something New and Non-proprietary!: The white paper advocates for an open-source approach to data standardization. By making data model architectures publicly accessible, the initiative aims to foster widespread adoption, enabling insurers to implement these standards at no cost and facilitating a more cohesive industry framework.openIDL

Extensibility: A Framework for All

A standout feature of the proposed openIDS framework is its inherent extensibility. Designed to be technology-neutral and adaptable, this framework is not limited to a specific segment of the insurance process. Whether it’s underwriting, claims management, actuarial analysis, or regulatory compliance, the openIDS framework provides a versatile foundation that can be tailored to various applications. As long as the data standards work through the governance of the working group, they can be extended.

This adaptability ensures that as the insurance landscape evolves—be it through the introduction of new products, regulatory changes, or technological advancements—the framework can seamlessly accommodate these developments.By eliminating proprietary barriers and promoting an inclusive model, the openIDS framework paves the way for enhanced collaboration, innovation, and efficiency across the entire insurance ecosystem.Linux Foundation

Conclusion

The openIDS white paper presents a compelling case for the urgent need for standardized data protocols in the insurance industry. By embracing an open, extensible framework, stakeholders can look forward to a future where data flows seamlessly, operational costs are reduced, and innovation thrives. For those interested in delving deeper into the specifics of this transformative initiative, the full white paper is available for review.

In a major step toward modernizing the insurance industry, openIDL (the open Insurance Data Link) has officially launched the openIDS Data Specifications Working Group — a collaborative effort aimed at revolutionizing how insurance data is standardized and shared across the sector.

This initiative comes at a pivotal time for carriers, regulators, and vendors alike, all of whom are navigating a rapidly evolving digital landscape. By introducing an open, shared data framework, the openIDS Working Group aims to break down data silos, foster meaningful collaboration, and unlock new opportunities for innovation and speed-to-market.

Why This Matters

The insurance ecosystem is filled with talented partners — from insurtech startups to legacy system providers — but too often, outdated data structures and inconsistent formats get in the way of collaboration. The openIDS Working Group is tackling this challenge head-on, creating a modern, flexible, and community-driven data standard that makes it easier to build together.

Key goals of the openIDS initiative include:

💡 Fuel Innovation: With a shared language for data, organizations can more easily build new tools, products, and services that work across systems and partners.

🤝 Simplify Vendor Collaboration: A common data standard reduces integration friction and shortens the time it takes to launch new solutions.

📊 Support Smarter Regulation: While not the sole focus, the framework also streamlines regulatory reporting by reducing redundancy and making compliance faster and more consistent.

⚙️ Increase Operational Efficiency: By eliminating duplicative data efforts, organizations can reallocate resources and improve accuracy.

Whether you’re modernizing core systems, testing new data partnerships, or simply tired of reinventing the wheel with every integration, openIDS offers a smarter, more scalable path forward.

Join the Conversation: April 21 at 4PM EST

If you’re a carrier, technology partner, regulator, or insurance innovator, we’d love to collaborate with you.

📅 The next openIDS Working Group meeting is April 21 at 4:00 PM EST. 📩 Message us to find out how to be invited to the meeting.

This is your opportunity to shape the future of insurance data and contribute to an open, interoperable foundation that benefits the entire industry.

About openIDL

openIDL is a Linux Foundation project that brings together stakeholders from across the insurance ecosystem to improve the way data is shared, secured, and utilized. Through open-source governance and community-led development, openIDL promotes transparency, trust, and innovation — while giving participants full control over how and when their data is used.

The openIDS community is excited to announce the release of our latest white paper, “The Case for Open Insurance Data Standards,” which delves into why the Property and Casualty (P&C) insurance industry is at a pivotal moment of rapid technology advances, increasing regulatory demands, market expectation shifts, and the extreme need for seamless and secure data exchange. Proprietary data formats have long dominated the industry, but they come with limitations—high costs, lack of interoperability, and vendor lock-in. Now, a new open-source initiative is poised to revolutionize how the industry shares and utilizes data.

This document lays out the urgent need for a universal, open, and non-proprietary data-sharing framework in the P&C insurance industry.

Key Highlights

Why Open Standards?

The insurance industry remains one of the few global sectors without widely adopted open data standards. Other industries, such as finance and healthcare, have reaped the benefits of standardization, including reduced costs, improved efficiency, and accelerated innovation. Now, it’s time for insurance to follow suit.

Open data standards offer numerous advantages, including:

Enhancing Interoperability – Creating a seamless exchange of data between carriers, reinsurers, brokers, regulators, and third-party providers.

Improving Transparency and Compliance – Providing regulators with more consistent and accessible data formats.

Driving Innovation – Enabling the development of AI-driven analytics, real-time risk modeling, and blockchain-based smart contracts.

What is openIDS?

openIDS is an open-source framework developed and maintained by the Linux Foundation, the world’s largest open-source development platform. This initiative is built on principles of transparency, collaboration, and long-term sustainability. Unlike proprietary systems, openIDS provides a flexible, extensible data standard that supports all lines of business within P&C insurance.

Key features of openIDS include:

A unified, future-proof core model that facilitates seamless data exchange across the insurance ecosystem.

An extensible framework that allows for customization while maintaining interoperability.

Compatibility with advanced technologies like AI-driven underwriting, blockchain contracts, and real-time risk analysis.

Support for multiple languages and global adoption, ensuring a broad industry impact.

Join the Movement

The adoption of open standards is a crucial step in modernizing the P&C insurance industry. We invite industry leaders, insurers, reinsurers, regulators, and technology providers to collaborate in shaping this transformation.

We encourage you to read and share this resource with colleagues and peers who may be interested in insurance data and data exchange transformation. Your feedback is valuable to us; please feel free to share your thoughts and questions after reading.

Stay tuned for Part II of this openIDS White Paper series and for more updates & resources as we continue to grow and support the industry.

Together, we can build a more efficient, transparent, and innovative insurance industry. Join the openIDS community today and be part of the future of insurance data exchange.

Why the Property and Casualty Insurance Industry is CreatingNew Open Standards for Information Exchange

The property and casualty (P&C) insurance industry is at a critical juncture. For decades, insurers, reinsurers, brokers, and third-party vendors have relied on proprietary data formats resulting in limited agility, inefficiencies, and increased costs. In an era where data is the cornerstone of competitive advantage now for every industry, these legacy constraints are no longer sustainable.

A shift toward open data standards presents a transformative opportunity. By collectively building and widely-adopting a universally accepted, non-proprietary framework for data exchange, the industry can enhance interoperability, streamline operations, and accelerate innovation. This white paper explores why the adoption of open standards is not just an option — it is an imperative for the future of insurance.

Abstract

Can you imagine a universal and widely-adopted data sharing process for the P&C industry? What if the only thing that needs to be done is “turning on the spigot” to allow other parties to receiveyour data as a feed across it through a query? Wouldn’t it be greatif a consensus-built format is open, non-proprietary, and futureproof?Can you see the opportunities in joining every other majorglobal industry in their mutual industry benefits resulting fromcollective contribution to open source platforms – that actually shiftbottom lines?

The Property and Casualty (P&C) insurance industry is undergoing significant

transformation as technological advancements, increased regulatory scrutiny, and market

demands for efficiency drive the need for seamless data exchange. Historically,

proprietary data formats have been widely used to facilitate communication between

carriers, reinsurers, and regulators. However, these formats often introduce barriers such

as high costs, lack of interoperability, and vendor lock-in. In contrast, free and open

standards offer a compelling alternative by providing universally accessible data

exchange protocols that enhance collaboration, reduce costs, improve transparency,

and foster innovation. Such standards should be non-proprietary and open through an

organization that has decades of proven success in open governance and the capacity to

maintain these frameworks and characteristics indefinitely. This paper explores the

benefits and value proposition of building non-proprietary and open standards in

comparison to proprietary and closed formats and frameworks – highlighting key

advantages in areas such as cost efficiency, scalability, regulatory compliance, and longterm

adaptability. openIDS (open Insurance Data Standards) is proposed as a launched

and currently functioning open standards framework-building project, built with,

supported, and managed by the Linux Foundation, the largest global open source

development platform.

The openIDS community seeks your support and participation in building the new and open

The insurance industry traditionally and historically benefits from operating behind closed doors, using proprietary systems and custom data formats. The benefits are shrinking and have created silos and increasing inefficiencies, unnecessary costs, and risks.

Meanwhile, every other major global industry has discovered the opportunities and proven solutions of open-source software (OSS), technology, and collaborative governance models to accelerate innovation, improve security, and reduce expenses.

With the rapid rise of AI and digital transformation, insurers are dipping their toes into open data ecosystems—leveraging APIs, external data sources, and machine learning tools—yet they are hardly contributing leaders, the overarching benefit to leveraging open platforms; nor does the industry have paired open standards, enabling these emerging technologies and systems to be leveraged efficiently, safely, and truly effectively.

“Over many years, new industries and thousands of organizations have entered the open source ecosystem. In the early days, some organizations leapt into OSS without a proper strategy and an execution plan; they did not emerge as winners. Others took a deliberative approach that embraced OSS methodology and engineering practices; they came out as leaders for open source activities in their industries or verticals.” – LF Research Guide to Open Source

Global non-profit organization, the Linux Foundation ("LF") is the largest open source operating system in the world.

The LF is governed, run, and maintained by its members, some of which are the largest global corporations including (but certainly not limited to as there are 14 Platinum, 17 Gold, 1,208 Silver, and 319 Associate members): AT&T, AWS, Cisco, Coinbase, Ethereum, Fujitsu, Google, Hitachi, Huawei, IBM, Intel, Meta, Microsoft, Oracle, Qualcomm, Samsung, Tencent, and VMware. Over 850 open source projects, 17,000+ contributing organizations, 777,000+ developers contributing code, and 76,300,000+ lines of code added weekly, the LF has and continues to maintain the beat of the world’s technological heart, openly.

This “take but don’t give” approach comes at a cost: without clean, governed, and standardized data, insurers risk feeding AI models with messy, inconsistent, inaccurate, and even dangerous information that leads to flawed risk assessments, regulatory penalties, lawsuits, reputational blows, and financial losses.

Innovation impact and ability to securely and effectively generate scalable products, services, and implementation of technological advancements to match the times has also been stunted by the industry’s under-involvement in open platforms.

Opportunities to leverage cross-industry partnerships for access to more and better data and existing global cross-industry digital advancements (think: IoT, real-time data exchange, quantum computing, and optimized security…) has also been diminished by sitting in the bleachers of complacency and de facto loyalty to restrictive systems.

“Today, OSS powers the digital economy and enables scientific and technological breakthroughs that improve our lives [and business]. It’s in our phones, our cars, our airplanes, our homes, our businesses, and our governments.

Organizations involved in building [technology / software] products, regardless of their specific industry or sector, are likely to adopt OSS and contribute to open source projects deemed critical to their products and services.”

The world is shifting toward data democratization, yet insurance companies continue to rely on outdated, closed systems that increase operational costs and slow down business processes. The industry’s long-held competitive advantage through exclusive data access is eroding, and those who fail to adapt will continue to face the increasing inevitable consequences.

Moving past current data standard and format reliances (holding the industry majority back from revolutionizing and innovating) will open doors to the next era of insurance data utilization.

Unfortunately, there has not been a solid and scalable alternative to build and host necessary participation and wide-adoption. This gap, the lack of a universal, non-proprietary insurance data standards-building platform, has now been solved with the inception of openIDS. 🚀

Next Step: Gather industry leaders to shape and build the new open standards!

Coming next: Why the Insurance Industry Needs Open Governance, the realistic approach to revolutionizing insurance data standards with open governance and a non-proprietary, open platform to collaboratively build

Data is a cornerstone of the property and casualty (P&C) insurance industry, driving informed decision-making and operational efficiency. It enables insurers to assess risk accurately, price policies competitively, and predict future trends. By leveraging data, companies can enhance claims management, improve customer experiences, and develop innovative products tailored to evolving market needs. In an industry built on mitigating uncertainty, data provides the insights necessary to remain agile, reduce losses, and foster trust with policyholders.

Industries establish universal standards for many things, including data, to increase efficiency in utilization, reporting, and sharing. However, within the U.S. P&C insurance industry, there are few widely adopted common data standards. This lack of standardization causes insurers and others to spend billions of dollars each year translating data into formats for regulatory reporting, catastrophe models, and a myriad of other transactions. The time and cost involved increases resistance for insurers to cooperate with regulators attempting to obtain data to inform constructive legislation and regulation.

With rising catastrophes and growing populations in high-risk areas, access to aggregate data is crucial not only to the insurance industry, but to the U.S. economy, which requires affordable and accessible insurance to function.

Why Does the U.S. Property & Casualty Market Have This Unique Problem with Data Standards?

The U.S. P&C insurance industry is regulated at the state level rather than by the Federal Government. There is overwhelming support among both regulators and insurers for state regulation, and it has been effective in many ways. However, with 50+ regulators and close to 4,000 insurance companies, it is almost impossible to gain a consensus on the need for data standards, much less the standards themselves.

The Association for Cooperative Operations Research and Development (ACORD) has attempted unsuccessfully to create and foster industry adoption of its data standards, both as a not-for-profit and now as a for-profit company. The National Association of Insurance Commissioners (NAIC), the primary body creating national consistency across states, has also worked on the issue for years to no avail.

Why Does It Matter?

The cost and difficulty of converting data to different formats increase the resistance of insurers to share data, especially with regulators. More importantly, converting data between architectures—like translating something from one language to another—can result in loss of clarity and accuracy. When insurers move from one Policy Administration System (PAS) to another, which happens frequently but is still hindered by the high costs of conversion, a key barrier is transforming policy data between different architectures.

Who Cares?

Insurers

Insurers acknowledge the problem, but no insurance association or vendor has successfully taken the lead to build a consensus on a solution. Many insurance executives may not fully realize the costs of lacking data standards, and those who do often feel powerless to address it. For carriers, the solution should create financial savings, enhance efficiencies, and increase the ability to leverage data in more creative ways.

Regulators

Insurer resistance to sharing data due to the associated cost and complication, combined with the lack of a data standard, makes it extremely difficult to create standards of performance from aggregated data that can inform constructive and consistent regulation. Consider that most of the Southeastern states required companies to file a data call for Hurricane Helene and Hurricane Milton losses. While the intent of each data call was the same, each one had a different format and slightly different requirements, increasing the costs and complexity of insurer compliance. Regulators ultimately represent consumers who are required to purchase insurance, as well as their state economies that require a healthy insurance market.

Third-Party Vendors to the Insurance Industry

Many vendors in the insurance industry recognize the challenges posed by the wide variety of data formats and terminology. They often invest significant resources assisting customers with data formatting and interpretation. As a result, quite a few vendors see this as a critical issue and are open to collaborating on a unified solution. Standardizing data would also make it easier for vendors to integrate with and transition between different companies, streamlining operations. However, some vendors may still view exclusive ownership of data models and architecture as a strategic business advantage.

What Might Work?

ACORD’s lack of success in creating a data standard proved that 1) there is no industry support for a not-for-profit organization that exists only to establish data standards, and 2) very few companies will pay for the use of a data standard.

The American Association of Insurance Services (AAIS) maintains proprietary data standards for stat reporting and data contribution for product development, like other Rating and Advisory Organizations do. However, as the only national not-for-profit Rating and Advisory Organization, its business model does not require it to protect that data architecture, which is simply a by-product of its business model. AAIS proposes to make its data model architecture “open source” so that others in the insurance industry can adopt it, in part or fully, at no cost.

How Will AAIS Make it Work?

AAIS was established as a not-for-profit organization with the goal of fostering collaboration among its insurance company Members. This collaboration enables insurers to develop better and more cost-effective solutions that benefit the entire industry—solutions that individual companies could not achieve on their own. In 2021, AAIS created a not-for-profit subsidiary under the Linux Foundation for insurance industry collaboration on data standards and reporting. The Linux Foundation is dedicated to creating and maintaining not-for-profit open-source industry standards with a proven governance framework that allows transparency and participation while ensuring that collaborative work product does not become compromised or proprietary. As a Linux Foundation project, openIDL (Open Insurance Data Link) is an existing platform that is governed by its time-tested governance model.

What Is AAIS’s Proposal?

AAIS will update its stat data model architectures, harmonizing them with existing open-source standards, such as OASISLMF and OMG, as well as others willing to contribute their data structures.

AAIS will donate its data model architecture to openIDL and the Linux Foundation as an open-source model architecture, available at no cost to anyone that would like to use it.

The maintenance and updating of the data model architecture would be owned and developed within the Linux Foundation through openIDL, with participation and support of interested parties in the insurance industry.

How Would the Industry Support and Participate In This Process?

Membership in openIDL follows the proven governance model used by countless industries. Any industry participant may become a member of openIDL and potentially serve on its board. Not-for-profit firms and regulators can join for free. Full memberships are calculated using a formula based on the number of employees, capping out at about $250,000 per year with a guaranteed board seat. A lower cost membership is available, priced from $10,000 to $50,000 per year, based on enterprise size, creating a class from which additional board members may be selected. Board members collectively govern the organization, and members have the right to participate in the development and maintenance of data standards.

How Would This Get Started?

The openIDL organization was originally developed as a data-sharing platform, created by AAIS and donated to the Linux Foundation, which required a standard data model architecture. While openIDL will continue to support its platform, its focus will shift to data standards. openIDL has funds to continue operations for approximately 12 months, but as AAIS shifts from the openIDL platform to focus on data, it will need to replace a few primary members to continue to fund and build consensus for open-source data standards. There is active interest from insurance regulators, insurance not-for-profits, industry third-party vendors, and some large insurers; efforts are underway to create critical mass.

If You Build It, Will They Come?

Good question! Adoption may be slow in the beginning, but over time, open standards often follow a predictable adoption course. In the initial stage, the adoption of open standards is expected to act as a baseline framework, serving as an intermediary for mapping data before converting it to another standard, like a universal translator. Incremental adoption is anticipated, such as in the case of the aforementioned catastrophe data call by multiple states, where the data standard provides a foundation for them to issue a standardized data call. Over time, creators of new policy administration systems will start integrating elements of the data model architecture, gradually driving broader adoption.

Why Should I Care About This?

The insurance industry plays a vital role in our economy and nation. While improving data flow may pose short-term challenges (each organization would define those challenges differently), the long-term benefits far outweigh the costs. As data becomes increasingly critical for accurate insurance processes, the industry must adopt data standards to manage larger volumes efficiently. Supporting this mission strengthens the industry’s future and upholds our collective responsibility to ensure its continued success.

Contact Information

For more information, please contact the following individuals.

SAN FRANCISCO, Jan. 28, 2025 /PRNewswire/ — Open Insurance Data Link (openIDL), a forward-thinking consortium focused on establishing critical data standards and leveraging blockchain technology to revolutionize data exchange across the insurance industry, is pleased to welcome new members reThought Flood and Cloverleaf Analytics. As members of openIDL, reThought Flood, an MGA leader in data-driven insurance solutions, and Cloverleaf Analytics, a pioneer in advanced insurance data analytics, will help openIDL lead the charge in insurance data standardization.

As active members of openIDL, reThought Flood and Cloverleaf Analytics will play a pivotal role in the newly launched open Insurance Data Standards (openIDS) Working Group, spearheading the development and adoption of open, non-proprietary, and universally accepted data standards. These efforts represent a critical first step toward building a transparent, and collaborative, data standard that can serve as a foundation for the industry’s future.

“We are pleased to welcome reThought Flood and Cloverleaf Analytics to the openIDL community,” said Josh Hershman, Executive Director of openIDL. “With their support and leadership, we hope to address the fragmented regulatory framework of the U.S. P&C insurance industry, which spans 56 jurisdictions and thousands of insurers, yet has made reaching a consensus on data standards elusive.”

The partnership underscores a transformative step toward addressing one of the industry’s most pressing challenges: the lack of widely adopted data standards in the U.S. property and casualty (P&C) sector. This absence of standardization costs insurers billions annually in translating data for regulatory reporting, catastrophe modeling, and operational tasks. These inefficiencies not only burden insurers but also hinder their ability to collaborate effectively with regulators and other stakeholders, obstructing efforts to create meaningful, informed policies. By adopting comprehensive data standards, the industry can enhance efficiency, reduce costs, and foster constructive collaboration between insurers, regulators, and other stakeholders.

“The value of participating in the openIDL and fostering open standards with openIDS is in building together what no one entity could build alone,” said Werner Kruck, CEO of the American Association of Insurance Services (AAIS). “By welcoming new members into the OpenIDL community, we open new avenues of collaboration to help shape the next generation of insurance data standards and governance. Through AAIS’ membership in openIDL, we look forward to working with the OpenIDL community to break down barriers and drive the adoption of transformative insurance data standards that will benefit the entire ecosystem.”

To learn more about openIDL, including how to participate in the community and become a member, please visit openidl.org.

Supporting Quotes

“reThought is very pleased to become a part of openIDL, a game-changing open source initiative of benefit to the entire insurance industry. As an MGA with significant reporting requirements to capacity partners, a truly open data standard would allow organizations to increase both the efficiency and the effectiveness of shared data and reports. Imagine a world where we all “speak the same data language”, it would be monumental.” Cory Isaacson – Founder and CEO, reThought Flood

“When I founded Cloverleaf in 2015, it was with a vision that the only way our industry would excel at digital transformation, was if data insights were delivered in a unified common language. We look forward to marrying our vision with openIDL as we strive towards a future where all insurers and regulators can access secure, meaningful data insights as seamlessly as turning on a light switch.” Robert Clark – Founder and CEO, Cloverleaf Analytics

“Cloverleaf is honored to collaborate with some of the nation’s leading insurers, regulators, and technology companies in joining the openIDL to guide the industry into an age of greater efficiency, data transparency and security, compliance, and growth. Just as insurers rely on robust data to make informed underwriting decisions, the openIDL will serve as the foundation for the entire insurance industry’s data-driven future, ensuring trust and reliability as we move towards more AI-driven business models.” Michael Schwabrow – EVP of Sales and Marketing, Cloverleaf Analytic

AboutopenIDL openIDL was founded by (AAIS) in 2021 as a Linux Foundation project. Building a Cohesive, Smarter, More Secure Insurance Industry. The project and its various initiatives were created for insurance industry collaboration on data standards and reporting. The Linux Foundation is the largest global open source software development non-proprietary platform focused on enabling industry-wide and cross-industry collaboration by means of the LF’s proven open governance model and framework. Generating and maintaining Industry Open Standards utilizing the framework of transparency, participation, and a strong governance model ensures that collaborative work and products do not become compromised and/or proprietary. openidl.org

About reThought Flood Founded in 2017, reThought Flood is a technology-centric Managing General Agent focused on US flood risk. reThought offers commercial and residential flood insurance on behalf of A.M. Best “A” rated carriers, and has formed strategic relationships with insurers, reinsurers, and other capacity providers to help them profitably innovate in the flood risk arena. reThought’s game-changing technology helps solve vexing industry problems underwriting flood risk, which requires advanced precision and a true understanding of the hazard. reThought has developed a state-of-the-art proprietary underwriting methodology and risk assessment technology which reflects the reality that with flood risk, inches matter. www.rethoughtflood.com

About Cloverleaf Analytics Cloverleaf Analytics is the leader in insurance intelligence solutions, having evolved from Business Intelligence (BI) into providing advanced tools using Artificial Intelligence (AI), Machine Learning (ML), Natural Language Processing (NLP), Speech to Insights, and other emerging technologies to empower carriers to achieve unparalleled growth. Cloverleaf enables carriers in diverse lines of business to create modern products that help insurers remain competitive against new market entrants while redefining what consumers and businesses understand as the meaning of insurance value. cloverleafanalytics.com

Media Contact Lanaya Nelson openIDL Phone: (860) 874-3491 Email: lnelson@openid.org

The importance of data within the insurance industry cannot be overstated. It IS the business. From risk assessment to pricing strategies, data serves as the backbone of decision-making processes. However, the industry has long grappled with challenges in data exchange and standardization, hindering efficiency, innovation, and profits.

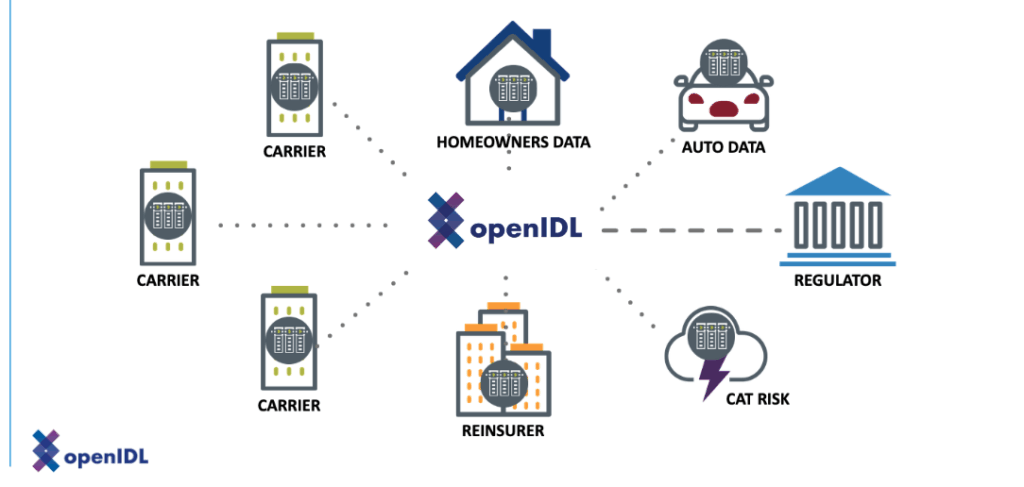

Open Insurance Data Link (openIDL), a Linux Foundation-hosted project and consortium, is poised to revolutionize how data flows within the insurance ecosystem. The openIDL community aims to build an open, secure, and permissioned data exchange network. To precede, openIDL must facilitate the establishment of stakeholder-agreed upon data standards. Once standards are set, the benefits of secure and efficient data exchange over the network are predicted to surface and bring tremendous change and opportunity to the industry.

At the heart of openIDL lies the simple yet powerful concept: improving data exchange between parties within the insurance industry. Although the network and its community are focused on the initial exchange use case between carriers and regulators, the success of this exchange will build the strong foundation for data exchange between any permissioned parties seeking a more secure, accurate, efficient, and robust mechanism that unquestionably trumps the common method used today: emailing spreadsheets.

Then, What is Standing in the Way? Stuck Standing at Standardization.

Another industry example of easier said than done. The big elephant in the room and primary requirement for the successful leap to better industry data exchange is the establishment of agreed-upon data data standards and models between stakeholders (i.e. competitors and regulators). Operating in such a highly regulated and competitive landscape, one in which risk aversion is the name of the game, it is no wonder expediency takes the back-burner to the delicate path to congruity between parties.

There are long-standing and understandable challenges in determining which data elements are necessary for regulators and convincing carriers of their importance, at times their necessity. Historically, determining the adequate data elements for regulators has been a point of contention and often leads to lengthy back-and-forth discussions and negotiations. Maintaining and balancing a marketplace is no small feat, but at what point does the pain of safely remaining in legacy become detrimental to the overall marketplace and its consumers? At what point does resisting cooperation and participation in the next industry era start to effect business bottom lines?

“I believe that having a better data exchange between carrier and regulator will make those markets stronger and will make them more efficient for the underlying carriers.” – Nick Lamparelli

openIDL addresses this stalemate challenge by providing a framework that minimizes debate and maximizes efficiency, allowing carriers to have agency in the next wave of regulation and the requirements that are tethered.

“What openIDL would be there for is creating the network and creating the standards for the exchange to take place… once we have the standard set up, there really shouldn’t be much adjudication involved as to whether or not this data should or shouldn’t be collected or distributed to the regulator [after the agreed-upon standards are established]. ” -Josh Hershman

With predefined standards in place, the focus shifts from debating data relevance to leveraging it for strategic advantage – benefitting all parties.

How to Tap Into the Power of Better Data Exchange

The leading fundamental use case for data exchange over the openIDL network between carriers and regulators will not only benefit regulators in gaining insights into market dynamics but will also empower carriers with clearer guidelines on data requirements. The result of building the network successfully will be in strengthening the overall market and enhancing efficiency and producing better data quality for both parties. Building successfully, though, is and has been a challenge. So, how can this be built successfully?

“…the only way we get there is having the network in place that underpins all of the flow of this data. That’s why I’m so excited about openIDL and the Linux Foundation in general.” -Josh Hershman

Step 1: Cultivate and engage the participation of a Robust Industry Stakeholder Consortium on a Truly Non-Proprietary and Trusted Platform enforcing the Proven Open Governance Model, the bedrock of great industry opportunity to follow.

Strep 2: Establishing agreed-upon Data Standards

Step 3: Developing on a strong, trusted, and dynamic open source technology platform to create a secure, permissioned data exchange network between parties.

The path:

Start with carriers-to-regulators

Next, move to broader application of Data Standards: while the initial focus is on data exchange between carriers and regulators, there’s recognition that data standardization can benefit various transactions within the industry. This includes interactions with reinsurers, MGAs (Managing General Agents), and other stakeholders (cross-industry).

Cross-Industry Standardization: participants acknowledge the potential for data standards to extend beyond the insurance industry, with examples cited from the automotive sector. Standardization across industries could lead to more efficient processes and better risk assessment.

Step 4: Additional Transformative Impacts: Pricing and Risk Assessment, New Use Cases for the Network and New Product Development

One of the most significant benefits of data standardization is its potential to revolutionize pricing and risk assessment. By harnessing near-to-real-time data from diverse sources, insurers can tailor products to individual needs with greater accuracy. Imagine a future where auto insurance premiums adjust dynamically based on driving behavior or homeowners insurance reflects real-time property usage—such possibilities are within reach. Also to mention new product development, more personalized features, and improved customer engagement and retention.

Beyond Regulators: A Holistic Approach

While the initial focus is on regulatory compliance, the implications of data standardization extend far beyond. From interactions with reinsurers to managing general agents (MGAs), standardized data protocols promise to enhance various facets of the insurance value chain. Moreover, the potential for cross-industry standardization opens doors to unprecedented collaboration and innovation.

“Nick, your point is spot on in the sense that if you have everything in some sort of distributed ledger and it just continues to live, it should ultimately make for a better, healthier marketplace. If you’re pulling in more data and you are engaged in the community and the network, at the end of the day you will also be more engaged with your customer. -Josh Hershman

Embracing the Future of Insurance

As we embrace the era of data-driven decision-making, initiatives like openIDL pave the way for a brighter future in insurance. By fostering a culture of collaboration and innovation, standardized data protocols empower stakeholders to navigate the complexities of an ever-evolving landscape. With every exchange of data, we inch closer to a more resilient, inclusive, and strong overall marketplace and a profitable, customer-centric insurance ecosystem.

In June, the Treasury’s Federal Insurance Office (FIO) released a report assessing climate-related risk and gaps in insurance supervision, Insurance Supervision and Regulation of Climate-Related Risks. The report represents another response to the Executive Order of President Biden back in May of 2021 with the objective to evaluate the challenges posed by climate-related risks to insurers and the regulatory efforts in place to help mitigate these challenges.

The FIO announced an initiative and a request for input from P&C insurers back in October for a proposed data call for climate-related data aiming to assess U.S. climate-related financial risks by collecting and analyzing data, specifically current and historical underwriting data on homeowners’ insurance at the Zip Code level.

The FIO’s recent report serves as a clarion call for a unified effort to address climate-related risks, fostering a more resilient insurance sector that can effectively safeguard individuals, businesses, and communities from the risks associated with a changing climate. It underlines the fact that climate-related risks are multi-faceted and ever-evolving, encompassing physical risks stemming from climate events, transitional-related risks related to shifts in technology and policies, and even litigation risks that could arise from these changes. As these risks become increasingly significant, insurance regulators are faced with the daunting task of ensuring the stability of the industry and its market in the face of environmental change and uncertainty.

By analyzing patterns in insurance claims, underwriting practices, and risk assessment, the FIO aims to better understand how climate-related factors are affecting insurance availability and affordability. This, in turn, will enable policymakers and regulators to make better-informed decisions to safeguard the financial well-being of Americans in face of climate change-related challenges and catastrophic losses. With consistent, standardized, granular, and comparable insurance market data, this will help assess the potential for major disruptions of private insurance coverage in vulnerable regions.

The P&C insurance industry plays a critical role in managing risk and providing financial protection to individuals, businesses, and communities. As climate change and its effects intensifies, insurers face the challenge of accurately assessing and pricing climate-related risks. The data collected by the FIO will contribute to a more comprehensive understanding of these risks, allowing insurers to refine their underwriting practices and develop products that address emerging risks. This initiative paired with industry participation and collaboration is likely to stimulate innovation within the industry as insurers seek new and impactful ways to manage and mitigate climate-related risks.

Collaborative Approach

The report highlights the commendable efforts made by state insurance regulators and the NAIC to integrate climate-related risks into their regulatory practices. However, it also emphasizes that these efforts, while a promising start, remain in the early stages of development and will require the help and participation of regulators, carriers, technology providers, and other climate-related entities.

To better understand the implications of climate-related risks for the insurance industry, as well as for the broader financial system, these groups need to work together to develop comprehensive strategies and a collaborative approach will be essential.

Tools and Processes for Enhanced Oversight

Existing regulatory frameworks offer state insurance regulators tools that can be adapted to incorporate climate-related risks. The report encourages regulators to prioritize the integration of these tools into their practices and procedures. Additionally, it recommends the creation of new tools and processes, such as scenario analysis and the utilization of NAIC’s Catastrophe Modeling Center of Excellence, to better assess and manage climate-related risks.

As the FIO continues its work to assess and support efforts in the insurance industry, there’s hope that the collaboration and strategies implemented lead to a more robust and adaptive insurance landscape–one that can weather the storms of environmental change and emerge stronger on the other side. The result will provide a broader picture of the insurance market landscape in regions particularly vulnerable to climate change impacts.

Challenges – For Both Public and Private

The FIO states that access to high-quality, reliable, and consistent data will be necessary for accomplishing each of its initial climate-related priorities. The challenge is the mechanism and operation of this data exchange and access ability. In the FIO’s October announcement of the proposed data call for climate-related data from insurers, they stated seeking input from carriers on:

Challenges to data collection, such as quality, consistency, comparability, granularity, and reliability

Key factors for developing standardized and comparable disclosures, as well as assessments of the standards provided by the Financial Stability Board’s Task Force on Climate-Related Financial Disclosures (TCFD) and the NAIC Insurer Climate Risk Disclosure SurveySuch assessments will include supervisory practices and resources, including:

data availability and integrity

Structural barriers to assessing, managing, and integrating climate-related risks (e.g., accounting frameworks, other standards).

Insurance Markets and Mitigation/Resilience – Assess the potential for major disruptions of private insurance coverage in U.S. markets that are particularly vulnerable to climate change impacts; facilitate mitigation and resilience for disasters.

“Such assessments will include examination of the insurability of disasters that are produced or exacerbated by climate change, including wildfires, hurricanes, floods, wind damage, and extreme temperatures.”

Treasury’s Federal Insurance Office Takes Important Step to Assess Climate-related Financial Risk – Seeks Comment on Proposed Data Call

For carriers, there are clear risks and challenges associated with the implementation of the FIO’s initiative. First and foremost is their and their respective insureds’ data protection, security, and its level of exchange/utilization transparency.

HOW? Permissioned Open Governance Network Model & Strategy

For both insurance regulators’ and insurers’ needs to be met effectively and securely, a true non-proprietary and non-profit intermediary is necessary. Trust and transparency will be paramount in this never-before implemented collaboration among these stakeholders to come to agreement on standardizations, frameworks, processes, and implementation.

The Linux Foundation’s proven and historically successful Open Governance Model provides the foundation for this needed collaborative effort to emerge and be maintained with equal agency and decision power, enabling all parties and stakeholders to meet their ultimate goals.

With the openIDL framework built on trust, transparency, and security, the use of DLT ensures information is secure and exchange of data is efficient, standardized, actionable, and accurate. The framework

enables insurance carriers to provide data to regulators in a standard and efficient manner while maintaining control over the data (their data never leaving their home)

allows community generation of a standard data format to promote interoperability and future adoption

stores the data in a cloud; each carrier has its own node, an analytics node, and an application for managing data calls (i.e. accept or reject calls for data)

provides network architecture using Hyperledger Fabric and other technologies such as Kubernetes and JavaScript/Angular UI to create transactions and management of data.

Data Privacy

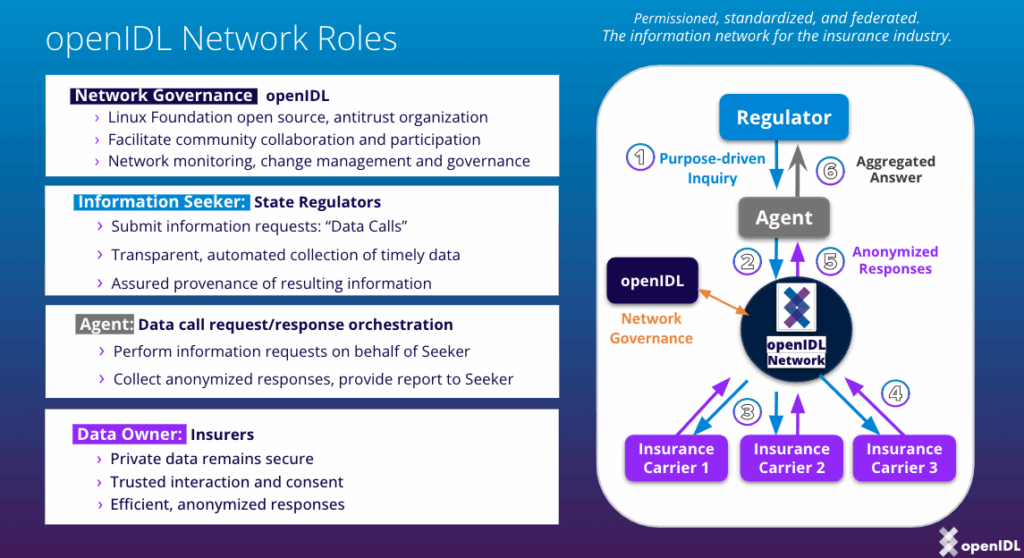

The primary challenge openIDL solves is the growing data privacy issue faced by insurance carriers. Carriers want to keep their data private and in their control, but if they constantly send data to regulators and other entities, control is inevitably compromised. openIDL allows carriers to provide data to regulators in a standard way while keeping the raw data in their cloud and only accessible through their node.

Standardization

openIDL implements data formatting, tokenization, and interoperability standards to ensure that multiple carriers can participate in the network. This will allow for future adoption and efficient data sharing, aggregation, and analytics applications.

Auditability

openIDL provides an auditable process for carriers to share their data with regulators and other entities. This visibility and transparency ensures that the data is managed properly and that carriers understand what will be done with their data.

Data Calls

openIDL provides a secure and efficient solution for regulators to conduct data calls efficiently and securely. The carriers respond to the data calls, helping regulators better monitor the market activity, plan for future emergencies, and protect consumers by providing data, and the results of the data calls are visible to the regulator through an analytics node. The first step in a data call is for the carriers to load their data into the harmonized data store inside their cloud. The data is then put into a standard format and is only accessible through their node. The regulator can access the data call results through an application that is part of a Kubernetes cluster. The Hyperledger Fabric API is used to create transactions and manage the data on the ledger.

As the initiative progresses and the data is effectively and securely collected and analyzed, we can anticipate a more resilient insurance sector better equipped to navigate the market challenges of a changing climate.

The insurance industry has arrived at the predicted inflection point between aligning its business with the technological advancements being leveraged successfully throughout other industries or staying put, carrying out business as usual, and slowly sunsetting one line of business at a time.

Common industry-wide challenges are expanding exponentially without viable solutions being implemented. Loss ratios are going haywire in certain lines of business, seen across every carrier’s reporting, yet each is trying relentlessly to solve for the losses within their own closed walls. Without a deliberate, collaborative effort among the various stakeholders (including carrier competitors), these shared challenges will continue to persist, and the alternative will likely be riskier in the long run.

The real catch-22 is that for carriers open to exploring solutions rooted in collaboration, the fruits of their labor have not yet been adequately matched in returns because these models require participation from peers and competitors to produce. These collaborative models epitomize “more the merrier” in that, the more carriers and relevant entities participate, the greater the impact of the network and, ultimately, carrier bottom lines.

So, what’s the hang-up? Trust, standards and governance, and the safeguarding of competitive advantage. The solution? An insurance-specific Open Governance Network.

What is an Open Governance Network?

The Linux Foundation (LF) is a non-profit organization and the world’s leading home for collaboration and open source software, hardware, standards, and data. Two years ago, the LF discussed the potential power and capacities of Open Governance Networks in a post, Understanding Open Governance Networks. The application of distributed ledger technology (DLT) is proposed as an efficient, secure, and scalable solution for highly regulated industries tackling shared challenges around data and its exchange.

Open Governance Networks enable a highly-regulated industry to form a group of stakeholders and competitors (a consortium) that governs itself in an open, permissioned, neutral, and participatory model. Over decades of facilitating the world’s most successful and competitive open source projects, the LF best practices and governance models have proven, time and again, the business advancements and scalability resulting from collaborative enterprise-level solution development.

A permissioned network consortium allows, upon consensus agreement, other organizations to participate and share operational, R&D-driven initiative, and development costs/software investments as well as sharing developed efficiencies, insights from data aggregation and analytics, and mutually-beneficial innovations leading to reduced time-to-market for individual products and services. Stronger security and data privacy standards, clear transparency, and increased data quality are inevitable outcomes through this network model’s governance.

Welcome to the decentralization of our evolving insurance industry.

openIDL and how it is different

As Open Governance Networks address the concern of neutral and distributed control in vertical industry use cases, there is no better organization than the LF to host and support the industry’s first of its kind, openIDL (Open Insurance Data Link).

openIDL is an insurance-specific and permissioned DLT-based project building a network that harmonizes industry data and secures the sharing of it both efficiently and transparently. The project was initiated in 2020 by the American Association of Insurance Services (AAIS), a member-governed insurance advisory organization in the United States that has been providing a common set of services for the insurance industry, such as regulatory reporting on a regional and national basis for the past 80 years. The network’s foundational use case, developed by AAIS, is regulatory and statistically reporting data exchange between insurers and state regulators/DOIs.

In 2021, the project was moved to the Linux Foundation to ensure a true member-premissioned open platform under the LF structured standards and governance model, free from proprietary solutions – as well as extensive member-exclusive benefits and support to drive project visibility, scalability, and success. The project’s use cases have since expanded, as well as its member community.

To date, openIDL’s member community includes carrier premiere members: Travelers, The Hartford, The Hanover, and Selective Insurance; state regulator and DOI members; infrastructure partners; associate members such as MOBI (Mobility Open Blockchain Initiative); and other non-profit organizations, government agencies, and research/academic institutions.

openIDL’s network is built on Hyperledger Fabric, an LF distributed ledger software project. Hyperledger Fabric is intended as a foundation for developing applications or solutions with a modular architecture. The technology allows components, such as consensus and membership services, to be plug-and-play. Its modular and versatile design satisfies a broad range of industry use cases and offers a unique approach to consensus that enables performance at scale while preserving privacy.

For the last few years, a running technology joke has been “describe your problem, and someone will tell you blockchain is the solution.”

As funny as this is, what’s not funny is the truth behind the joke, and the insurance industry is certainly one that fell head over heels for the blockchain hype. Like any revolutionary technological advancement throughout history, blockchain and DLT are no different. Failing always smarts in the beginning, but the learnings, iterations, and refinements eventually lead to strong problem-solution alignment. Timing is key. The other key is in the (sometimes long) process of dissecting the problem and coming to the best solution – not in having a solution and searching for a problem.

In recent years, there has been a dramatic and continuous increase in the amount of relevant – and timely – data needed and collected within the industry due to the proliferation of:

IoT devices, cloud adoption, and 5g network expansion

Increased insured connectivity adoption

Evolving climate-related risks and new related external data channels

Data needed for parametric and embedded product development

The growing strategic need for cross-industry data exchange and standards development

New data requirements and requests from regulatory and government entities

The remaining long list of increased-data-collection catalysts

With this increased need and in volume, the possibilities of utilizing these data has also skyrocketed in areas such as underwriting, risk assessment, marketing, segmentation, pricing accuracy, fraud detection, closer to real-time exchange, and many other areas within both carrier business and operations strategies. Inevitably, new challenges affecting all carriers are increasing proportionally, highlighting the need for a secure, private, and transparent platform for exchanging data.

AAIS predicted this need and recognized permissioned-DLT as an aligned solution to these shared industry challenges. The advisory organization saw this need for the “neutral ground” of a decentralized network- a consortium with a leveled playing field maintained by an organization dedicated to the health and growth of the network; not controlled by one company or organization.

With great process, planning, and framing through extensive industry expertise, openIDL was launched and hit the ground running to prove the concept of an industry permissioned network securely managing and exchanging information, held accountable by the LF Open Governance Network model, and able to keep up with the rapidly evolving risk landscape.

The openIDL Open Governance Network

Working to solve shared industry challenges, such as data privacy and standardization, that could not be solved by one entity alone and will open up doors for other innovation priorities and product development.

Enables insurance carriers to provide data to regulators in a standard and efficient manner while maintaining control over the data.

Community generation of a standard data format to promote interoperability and future adoption.

The data is stored in a cloud; each carrier has its own node, an analytics node, and an application for managing data calls.

Network architecture uses Hyperledger Fabric and other technologies such as Kubernetes and JavaScript/Angular UI to create transactions and manage the data.

Why the insurance industry needs an Open Governance Network

There have been many attempts to produce a functional, efficient, and secure industry data-exchange network. However, without trust, the risks are too high, and we all know what the business of insurance is rooted in.

This is precisely where the LF Open Governance Network model establishes the needed trust that has been lacking – and from the get-go. The power of both the Linux Foundation and its proven secure framework, as well as the trust, transparency, and security is intentionally woven into Hyperledger Fabric, providing a platform for carriers and all industry stakeholders to solve challenges while trusting in the governance of the community.

Challenges Solved by openIDL

Data Privacy

The primary challenge openIDL solves is the growing data privacy issue faced by insurance carriers. Carriers want to keep their data private and in their control, but if they constantly send data to regulators and other entities, control is inevitably compromised. openIDL allows carriers to provide data to regulators in a standard way while keeping the raw data in their cloud and only accessible through their node.

Standardization

openIDL implements data formatting, tokenization, and interoperability standards to ensure that multiple carriers can participate in the network. This will allow for future adoption and efficient data sharing, aggregation, and analytics applications.

Auditability

openIDL provides an auditable process for carriers to share their data with regulators and other entities. This visibility and transparency ensures that the data is managed properly and that carriers understand what will be done with their data.

Data Calls

openIDL provides a secure and efficient solution for regulators to conduct data calls efficiently and securely. The carriers respond to the data calls, helping regulators better monitor the market activity, plan for future emergencies, and protect consumers by providing data, and the results of the data calls are visible to the regulator through an analytics node. The first step in a data call is for the carriers to load their data into the harmonized data store inside their cloud. The data is then put into a standard format and is only accessible through their node. The regulator can access the data call results through an application that is part of a Kubernetes cluster. The Hyperledger Fabric API is used to create transactions and manage the data on the ledger.

Conclusion

openIDL is an important initiative for the insurance industry as it provides a secure and transparent platform for exchanging information, data, technology, and leadership Open Governance Network strategy.

The use of DLT ensures information is secure and exchange of data is efficient, standardized, actionable, and accurate. The Linux Foundation’s involvement is paramount as it provides the foundational and successful open governance model – free from proprietary uses — allowing carriers to solve industry-wide challenges collaboratively and securely.

openIDL represents a huge milestone for the industry at large. The network’s use of enterprise-scale permissioned-DLT and its commitment to data privacy and standardization makes it a viable solution for the industry moving forward. openIDL is perfectly positioned to bring everything we, the insurance community, have been discussing and planning for years.

It’s time to bring the plans to fruition and beyond, together.

For more information or to inquire about membership options & benefits, please reach out! info@openidl.org